Simple and Professional Guide to GST Cancellation

Introduction to GST Cancellation:

GST registration can be voluntarily cancelled if a business is dormant or falls below the required turnover.

Additionally, a GST officer may cancel registration due to non-compliance. Once cancelled, the entity is

relieved from filing GST returns and any associated tax payments.

Voluntary GST Cancellation:

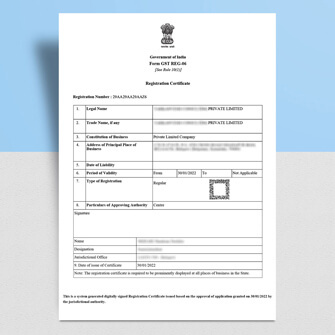

Entities wanting to voluntarily cancel their GST registration must submit Form GST REG-16 to the GST Department.

Upon approval, the GST Officer issues an order for cancellation (Form GST REG-19). Common reasons for voluntary

cancellation include business discontinuation, transfer, amalgamation, change in PAN, or turnover falling below

the threshold.

Benefits of voluntary cancellation include saving the business owner from the hassle of monthly GST return filing

and penalties.

Cancellation by GST Officer:

A GST Officer may initiate cancellation if a taxpayer continuously fails to file returns, doesn't commence

business within six months (for voluntary registration), violates GST Act or Rules, or obtains registration

through deception. The Officer issues a show-cause notice (Form GST REG-17) and provides an opportunity for the

taxpayer to be heard.

The taxpayer's response could lead to dismissal (Form GST REG-20) or cancellation (Form GST REG-19) of

registration. Non-compliance can result in penalties and a cascading effect on subsequent returns.

Procedure for GST Cancellation:

Vyapar Samadhan can assist in the online GST cancellation process. Before initiating, overdue GST returns must

be filed to ensure compliance. The cancellation application (Form GST REG-16) includes contact details, reasons,

desired cancellation date, and particulars of stock and returns.

Within 30 days, the GST Officer reviews the application and issues an order (Form GST REG-19) with an effective

cancellation date.

Final Return:

After cancellation, a final GST return (Form GSTR-10) must be filed within three months of cancellation or the

cancellation order, whichever comes first. This ensures no pending GST dues.

Preparing for Cancellation:

Before cancellation, clear any overdue GST liabilities and remit input tax on stock. The input tax credit on the

current stock must be repaid.

Rejection of Application:

An application may be rejected if incomplete or new entity registration is pending. The Officer communicates the

discrepancy, allowing the applicant to respond within seven days.

Revocation of Cancellation:

Taxpayers can apply for revocation within 30 days of cancellation. If satisfied, the Officer issues Form GST

REG-22; otherwise, Form GST REG-05 is issued, with reasons documented.

Benefits of Voluntary Cancellation:

Voluntarily cancelling GST registration is crucial to avoid compliance issues. It ensures the business owner

remains eligible for future registrations and simplifies the process.

Conclusion:

Maintaining GST compliance is vital, and voluntary cancellation, when necessary, streamlines the process. Vyapar

Samadhan offers support to navigate the complexities of GST cancellation, ensuring a smooth and compliant

transition.